Almost a decade after the demolishing of Empress Market’s surrounding areas, auctions seem to have made a strong comeback thanks to the successful sale of Pakistan International Airlines. Big business groups throwing around bigger numbers in a battle of egos live on television surely makes for some spectacle. It probably inspired PSL, which first conducted live bidding for franchises and subsequently switched from drafting to auctions for players as well, bringing yet another dimension of entertainment in the sport. However, the most meaningful auction of our times — spectrum — took place behind closed doors without any dramatic flair, even if its impact on economy is possibly more profound than anything else.

On March 10, the Pakistan Telecom Authority put up for sale almost 600 MHz of spectrum – more than twice the current levels. The auction had been years in the making, with the industry repeatedly pushing for better terms and more favorable pricing to avoid a repeat of the largely unsuccessful 2021 auction, where poor uptake left significant spectrum unsold. Read our deep dive into the information memorandum here to understand the key mechanics and pricing.

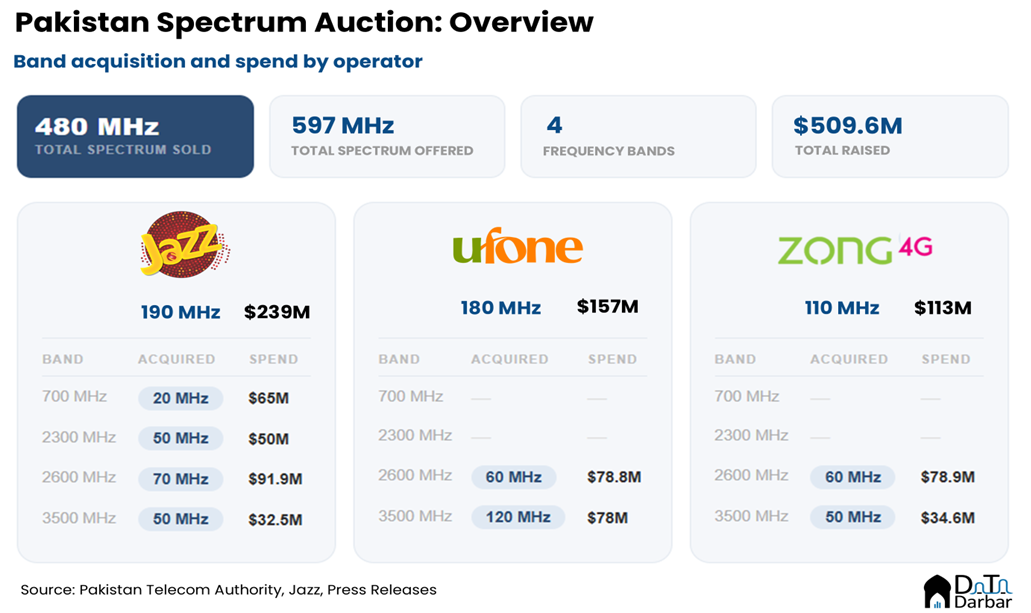

Three rounds and $507M later, the auction cleared 480 out of 597 MHz on offer. The mid-band 2300 MHz and 2600 MHz lots sold out entirely, reflecting strong operator confidence in those frequencies. The 700 MHz and 3500 MHz bands — important for wide-area coverage and 5G respectively — saw partial clearance, suggesting measured but genuine demand. The legacy 1800 MHz and 2100 MHz bands, however, attracted no bids at all, signaling a clear industry shift toward newer, more future-ready frequencies rather than reinforcing older infrastructure.

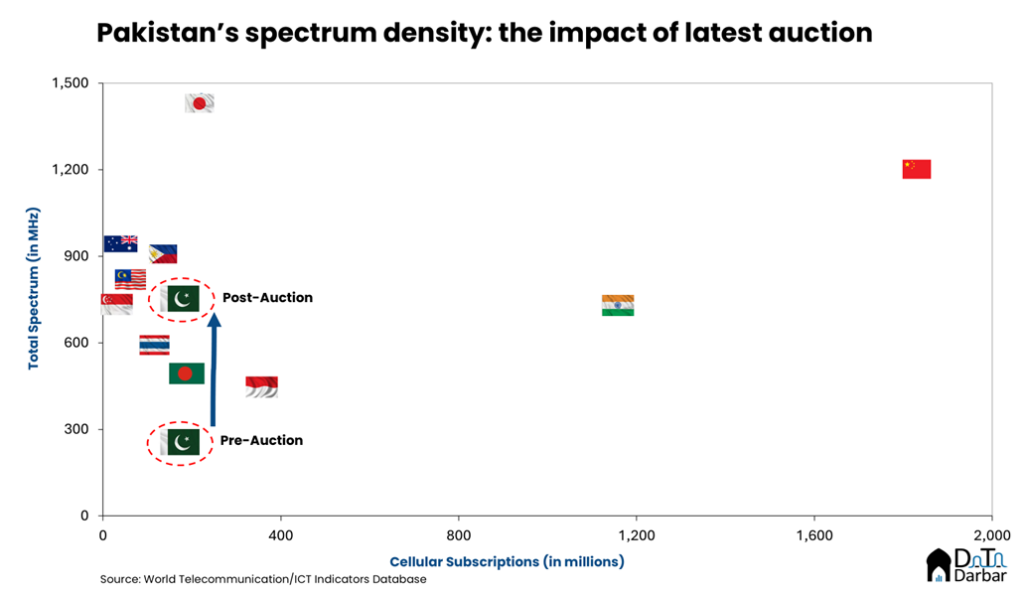

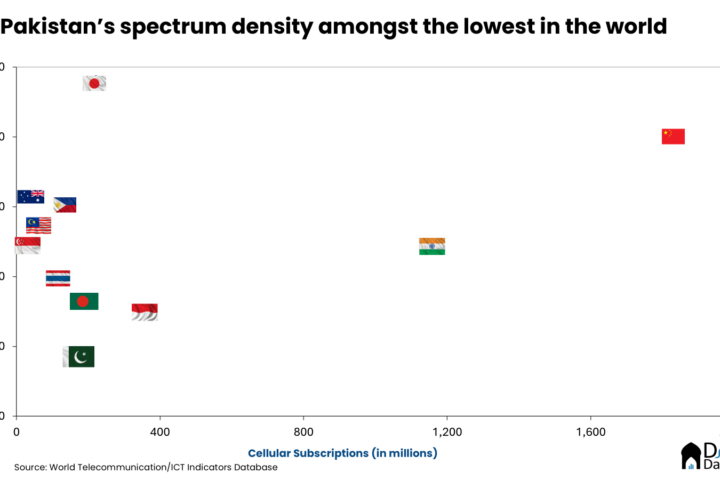

Consequently, Pakistan’s total available spectrum more than doubled overnight, a significant milestone for a market that had long lagged regional peers. While not every band cleared, the results represent a meaningful step forward for the country’s connectivity ambitions and lay a stronger foundation for the next phase of mobile network investment.

Making sense of operator strategies

Jazz bets big on breadth

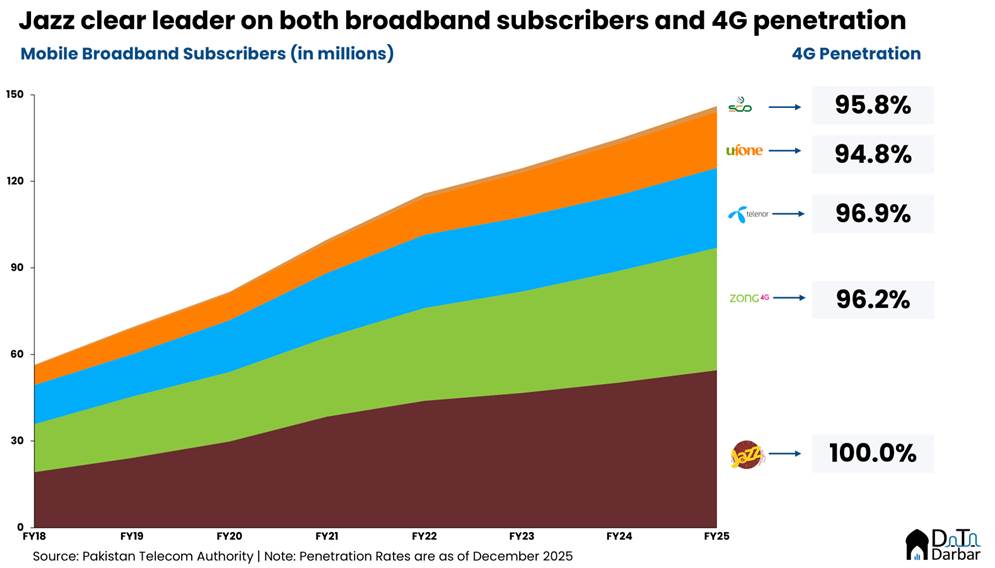

Jazz paid the most and bought the widest portfolio, becoming the only operator to acquire spectrum across all new bands. The wide mix is consistent with its leadership position, commanding almost 37% share in cellular and mobile broadband each, with 74M and 56M subscribers as of December 2025, respectively. In a LinkedIn post, CEO Aamir Ibrahim expressed excitement about the acquisition of 700 MHz band in particular, for being pivotal to closing Pakistan’s digital divide “as it enables us to extend reliable, high-quality connectivity across vast geographies, particularly in rural and underserved communities.”

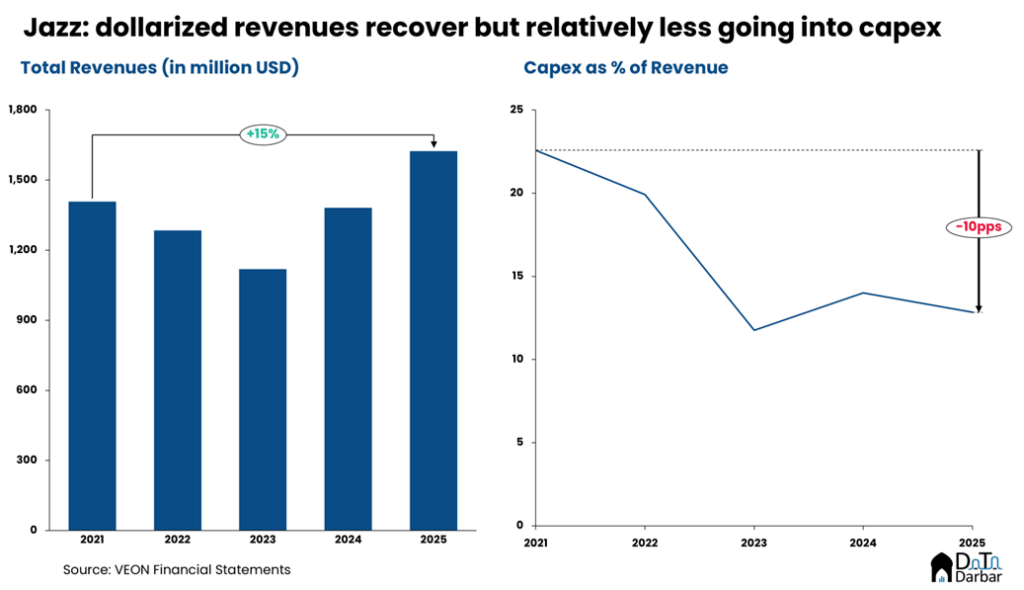

The company acquired 190 MHz for $239M in the latest auction, taking its total spectrum holdings to over 280 MHz. The strategy seems broad-based where Jazz is looking to; expand rural coverage; cater to the critical mass through higher-speed 4G; and roll out 5G in select urban centers, for which the first pilot has already been done. In a separate press release, the telco shared plans to invest $1 billion over the next three years to increase network capacity and modernize infrastructure. This would mark a steep acceleration in Jazz’s capex, which has averaged $222M (or 16% of revenues) annually between 2021 and 2025.

Ufone goes all-in on 5G

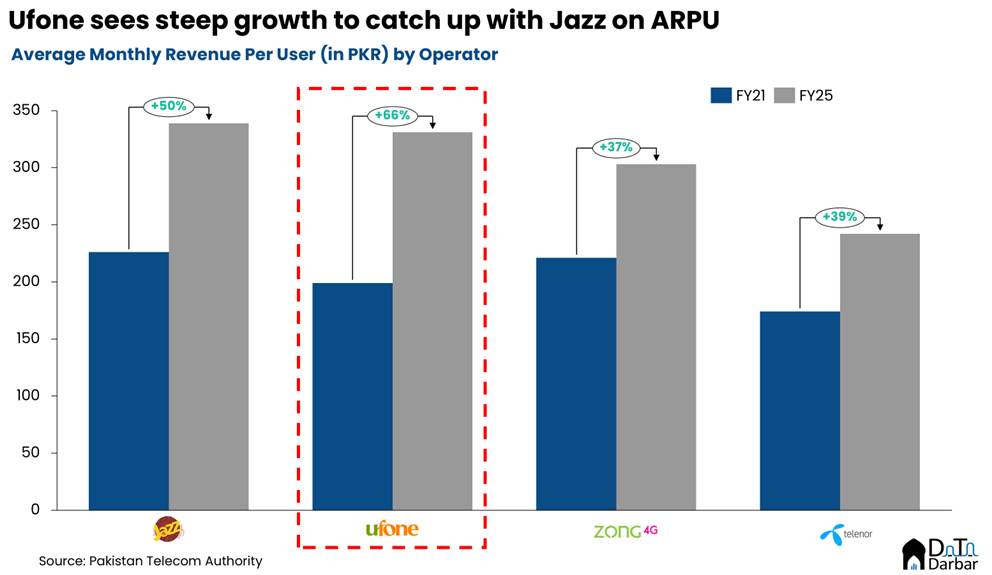

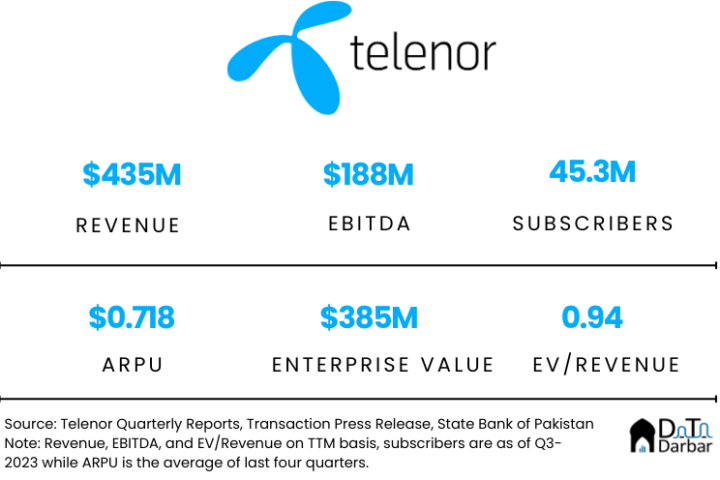

Ufone’s bet is quite interesting too for it emerged as the largest acquirer in the 3,500 MHz band with 120 MHz, more than the other two operators combined. In retrospect, one can obviously rationalize it within the context of merger with Telenor, which together boast some 49M broadband subscribers as of 2025 end. Keep in mind that it was also the only telco to participate in the 2021 auction and finally entering the 4G race, after years of missing out from the sidelines.

However, in recent years, it has aggressively tried to close the gap with other telcos. The progress is visible in the 4G penetration rates, where Ufone now stands at 95%, approaching the industry average of 97.8%. Till FY23, it was the only operator below 90%, even behind SCO. More impressive has been the group’s growth in average revenue per user (ARPU), increasing by 66% since FY21 to reach PKR 331, compared to the mean jump of 47.8%.

Now it wants to double down on 5G. “Our priority is to build a resilient and future-ready digital infrastructure that supports Pakistan’s rapidly evolving digital economy. With 5G, customers will experience more intelligent services, businesses will gain powerful new tools for productivity and innovation, and entire industries will be able to reimagine how they operate in a digital world,” notes Hatem Bamatraf, President and Group CEO, PTCL & Ufone, said. The positioning is also in line with their sub-brand, ONIC, that has tried to cater to digital natives through data-only packages with higher limits and better pricing.

Zong plays it safe

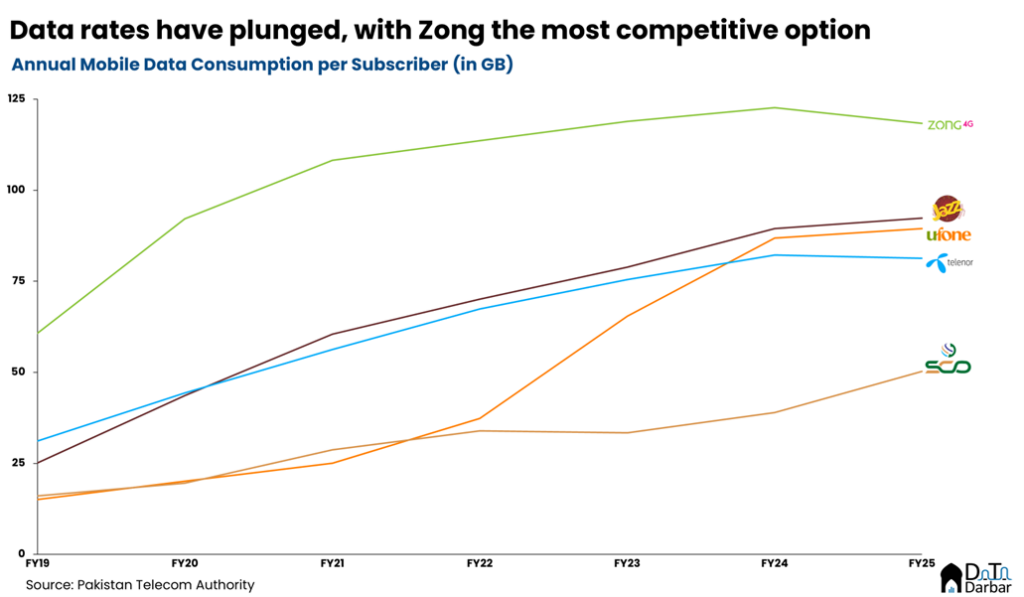

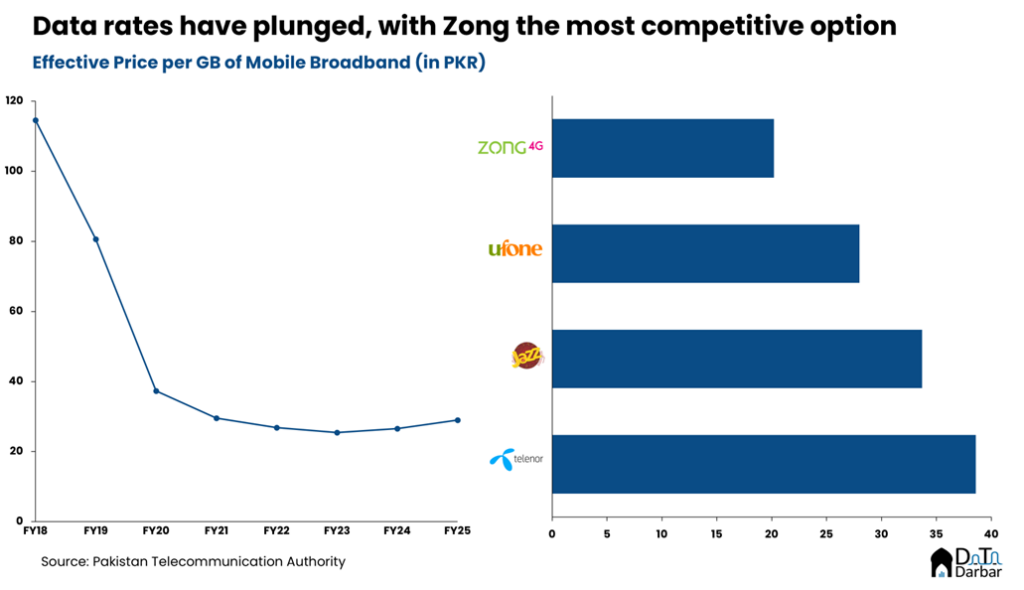

On the other hand, Zong bought and spent the least: 60 MHz of 2600 MHz and 50 MHz of 3500 MHz for a grand sum of $113.5M. This is at least a bit surprising because the telco has long been perceived a market leader when it came to mobile data and until FY24, boasted the highest 4G penetration rates. To this day, the Chinese telco is way ahead of others in terms of mobile data consumption per subscriber, at 118GB in FY25. No one else is in three digits. While the gap remains, things are far from hunky dory as the mean consumption declined 3.5% on a sequential basis, faring the worst in terms of rate of change.

There are other signs of concern as well: between FY21 and FY25, Zong has witnessed the slowest growth in ARPU at just 37.1% – trailing the industry average by a whole 10 percentage points. Admittedly, the underlying reason here may have more to with own intent than ability for the Chinese telco has positioned it products most competitively, offering the lowest effective price per GB of mobile broadband at just PKR 20.2. Whatever the case, the same aggression wasn’t visible in the spectrum auction.

The harder part begins

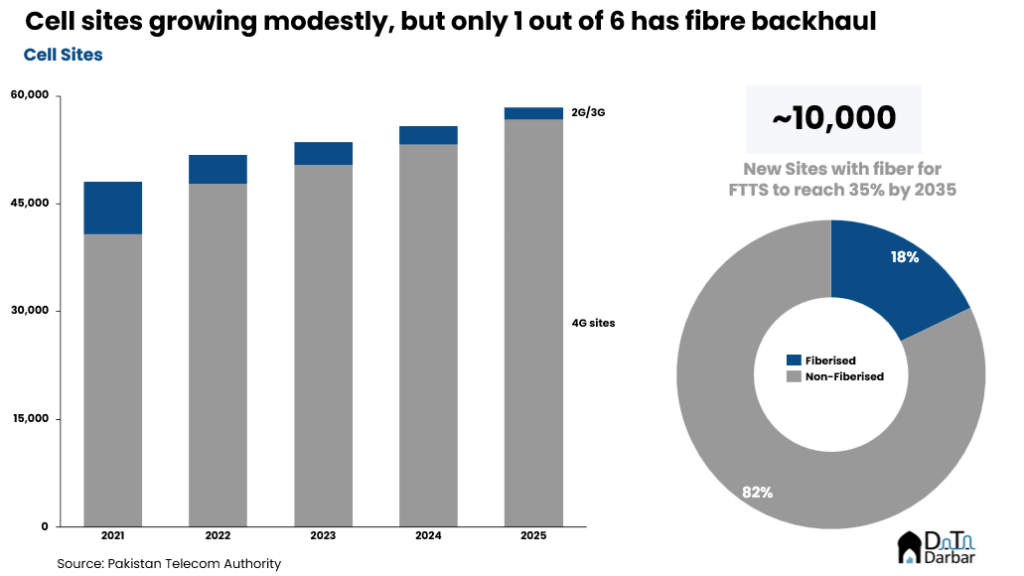

Now that spectrum availability has been addressed, the harder part begins. On the supply side, total cell sites have grown to 58,423 in 2025, with 4G coverage following behind. Fibre backhaul too has improved to 17.9% over the same period, albeit not quite at the required pace. The information memorandum sets a 35% fibre coverage target by 2035. It won’tbe cheap: fiberising a single site costs $10,000-20,000, thus translating into a hefty capital commitment.

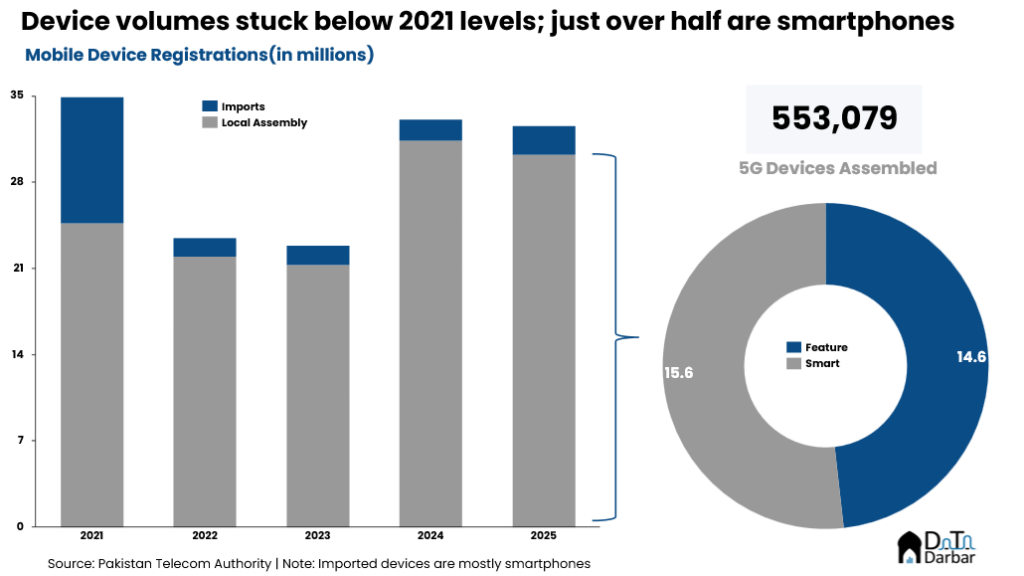

On the demand side, the biggest problem is dearth of 5G handsets. In 2025, only 1.8% of the locally assembled phones (or 3.5% of smartphones) were 5G-enabled. Priced upwards Rs60,000-70,000, these devices are relatively more expensive than what an average Pakistan can afford.

Naturally, this has serious implications for the operators’ potential payback period, which is only complicated by the industry’s low ARPUs. It’s more of a chicken and egg problem. Without the required spectrum, there was virtually no incentive for demand and supply sides to go for 5G devices, which skews the project economics of deployment for telcos. To help break through this loop, a push was needed and that’s exactly what this auction was all about.

Jazz’s 5G strategy has been inconsistent—they initially delayed rollout citing low handset availability, yet after launching, they still lack support for iPhones, exposing poor planning and execution.

It’s interesting to see how it’s work in North area of Pakistan i.e Kon, Kashmir and of course GB .area.

In these Mounting area Speed and Signals always issue .and UFone square Telenor then see what we found out