For the past several months, Pakistan has been unusually prominent in global foreign policy conversations. Islamabad’s careful cultivation of ties with the Trump administration culminated in its role brokering a ceasefire between Tehran and Washington and hosting the first direct negotiations between the two countries in decades. That closeness to Washington has been talked about at length, and attributed to many factors, including the deliberate embrace of crypto, an area where the Trump family has significant commercial interests.

The domestic regulatory push that followed was rapid by any standard. The Pakistan Crypto Council was stood up, a virtual assets ordinance created the basic legal infrastructure, and PVARA was established as the statutory authority responsible for licensing and oversight. Throughout this period, however, the State Bank of Pakistan remained largely on the sidelines — cautious, measured, and in no visible hurry to bring virtual assets into the formal banking system.

That changed yesterday. SBP’s BPRD Circular Letter No. 10 of 2026 replaces the 2018 prohibition that had blocked banks from facilitating any crypto-related activity, a restriction that had pushed the market into a legal grey zone dominated by P2P merchants operating without formal oversight. The new circular does not open the banking system to crypto unconditionally; rather, it creates a narrow, regulated channel available only to firms licensed by PVARA. The central point is that virtual-asset activity may interface with the banking system only where it is licensed, supervised, and traceable.

How the banking relationship opens

For a VASP, access to banking rails is staged, with the phases somewhat similar to what SBP’s own regulated entities undergo. A firm begins with a PVARA no-objection process. If it is granted, the applicant can move ahead with anti-money laundering registration, incorporation of a local entity, and a limited-purpose bank account used only for completing the remaining licensing formalities.

Full transactional banking begins only after the firm secures a full PVARA licence and the bank independently verifies that status. Even then, the bank is not simply opening a standard operating account. It must conduct enhanced due diligence, recalibrate its customer risk model, and monitor the relationship on an ongoing basis.

The key operational structure is the client money account, or CMA. This is a segregated PKR-denominated account held for customer funds, ring-fenced from the VASP’s own capital, non-remunerative, unusable as collateral, and outside the scope of ordinary cash handling. In effect, the circular is trying to ensure that customer rupees sit in a safeguarded banking layer even while trading activity happens inside a licensed digital-asset intermediary.

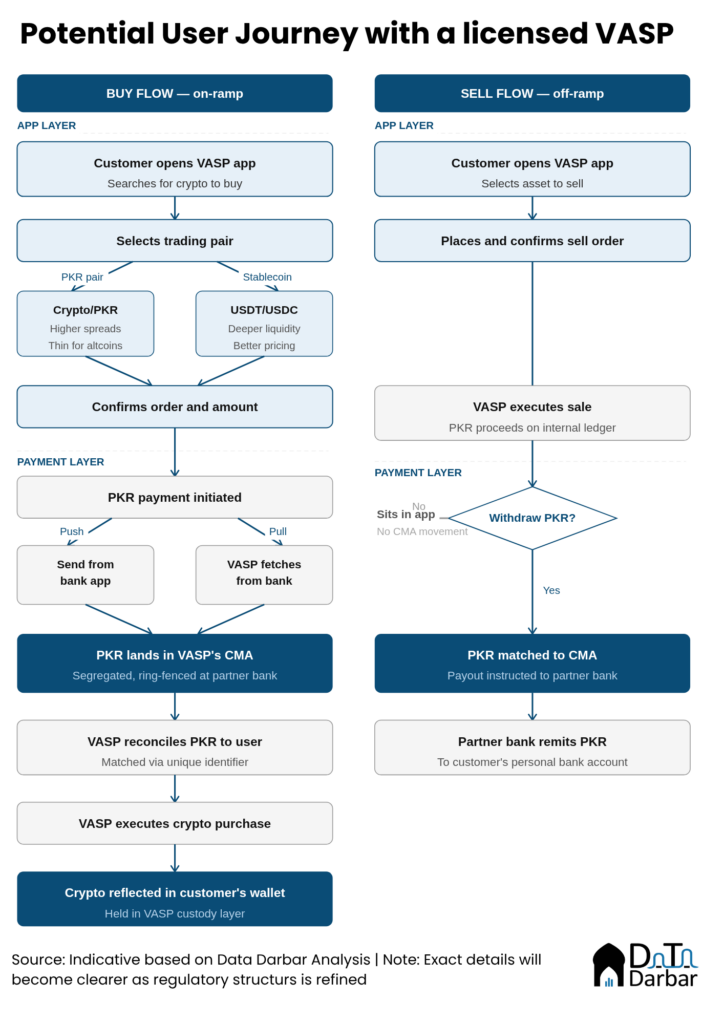

How it could reshape user experience

Buy Flow

The first diagram makes the customer on-ramp leg much easier to understand. It shows that the app interface and the payment architecture are related but distinct. The user interacts with the VASP app, but the rupee funding leg still resolves through the banking system and lands inside the segregated CMA before the crypto purchase is executed.

Two features in the buy flow stand out. First, the customer may see more than one execution path inside the app. In some cases a platform may offer a direct crypto/PKR pair. In others, especially where global liquidity is deeper in stablecoin markets, the effective path may be PKR into USDT or USDC and then into the selected asset. From the customer’s perspective that can affect pricing, spreads, and asset availability.

Second, funding can occur through either a push model or a pull model. In a push model, the customer initiates the transfer from a bank app. In a pull model, the instruction is initiated within the VASP interface and the funds are fetched from the linked bank account. In both cases, the operationally important moment is the same: PKR lands in the VASP’s CMA at the partner bank, is reconciled to the customer through a unique identifier, and only then is the crypto purchase executed.

That sequencing matters because it clarifies what the bank is and is not doing. The bank is settling and safeguarding rupees. It is not warehousing the virtual asset, deciding which token the customer buys, or operating the exchange logic. Those functions remain inside the licensed intermediary.

Sell Flow

The second diagram clarifies the off-ramp. It shows that a sale of crypto does not automatically mean immediate bank payout. The trading event and the bank remittance event are linked, but they are not the same thing.

When the customer sells a virtual asset, the VASP executes the transaction and records PKR proceeds on its internal ledger. At that point the customer may leave the proceeds inside the app wallet rather than move them out immediately. The diagram correctly separates that internal balance state from the formal bank payout leg.

Only once the customer chooses to withdraw PKR does the process move into the CMA-based banking workflow. The VASP matches the customer’s rupee claim to the safeguarded CMA pool and instructs the partner bank to remit funds to the customer’s personal bank account. That means the bank’s role appears at the point of rupee settlement, not at the point of trading execution.

This distinction is important for both regulation and user expectations. It reinforces that the platform wallet and the bank account are not identical things, even if they are connected by a licensed settlement process. It also gives regulators a clearer audit trail: trade execution remains inside the supervised VASP, while fiat entry and fiat exit become visible at the banking layer.

What changes for market structure

These mechanics could reshape who captures value in Pakistan’s digital-asset market. Large platforms such as Binance benefit if they can move from preliminary regulatory recognition to full local licensing, because the circular now offers a lawful route to PKR settlement, smoother customer funding, and greater institutional credibility. A properly licensed exchange no longer has to rely entirely on external merchant liquidity for the rupee leg.

That creates pressure on the grey market. Unlicensed P2P merchants have long mattered because they solved the fiat conversion problem. Once licensed VASPs can connect users to safeguarded bank-based rupee channels, part of that role may shrink. The business does not disappear overnight, but its strategic importance changes because the formal market begins to internalise a function that the informal market used to dominate.

The same shift could create openings for other regulated financial intermediaries. Liquidity providers, broker-style firms, and even existing money changers may try to enter the perimeter where rules permit, especially in areas related to fiat conversion and settlement support. Much will depend on how PVARA defines licence categories in practice and how willing banks are to support different types of licensed firms.