It gets a bit boring to write the same thing time and again, but as far as digital payments are concerned, the story isn’t gloomy at least. The exact opposite, in fact, even as most people don’t grasp the extent of how far things have come. According to the State Bank’s latest review, 92% of the retail transaction volumes have been digitalized, excluding branchless.

Since it includes channels like ATM, we believe this figure to be fairly inflated and not a great barometer for assessing true digitization. Instead, we prefer to use the adjusted share of digital payments in retail banking transaction activity. Before diving into the details, let’s take a moment to understand the underlying data. First is the paper-based instruments such as over-the-counter cash deposits or demand drafts. Then you have PRISM, a high-value real-time gross settlement system, with only 59 participants. This is what banks use to send proceeds among themselves, or how money flows into government securities. Until recently, the SBP also used to classify real-time online branches under e-banking. Its current definition of digital payments includes:

- ATM

- Internet banking

- Mobile Banking

- Call Center/IVR

- Point of Sale

- E-commerce

- E-wallets

There are two big drivers of digital payments which aren’t included either in the SBP’s 92% or our own adjusted indicator: branchless and digital banks. The former operates on a whole another scale and with the transition of Easypaisa to the latter, there might be some confusion in the coming months. But for now, in order to maintain consistency, we will leave them out and unlike the regulator, focus exclusively on scheduled banking, as it was before 2025, thus leaving out EMIs. And there too, specifically the channels that are digital at the user level i.e. leave out ATMs.

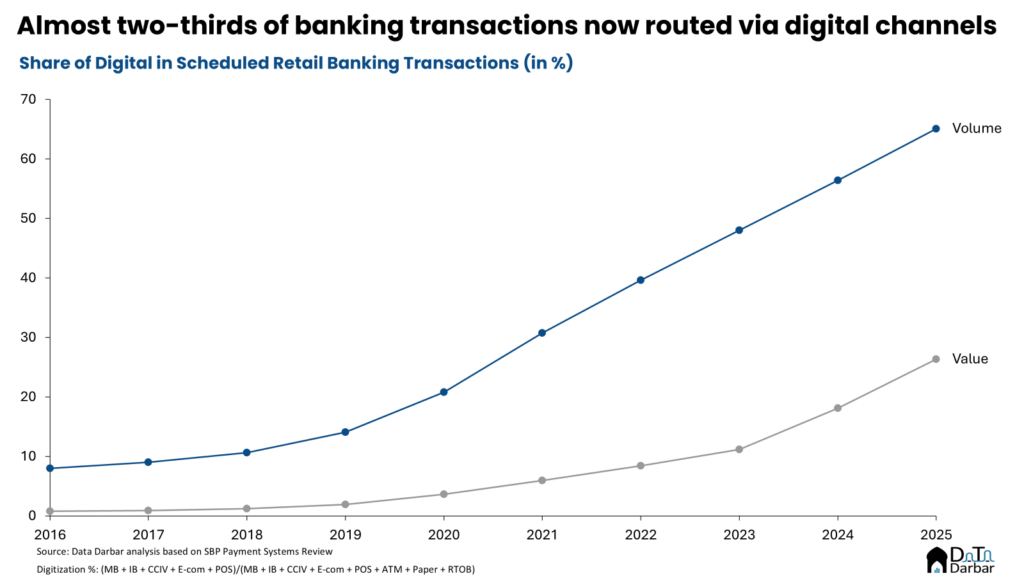

According to the adjusted indicator, 67.4% of all scheduled banking transaction volumes had been digitalized in Q2-FY26, up 7.49pps YoY. Put another way, people are wholeheartedly embracing online payments at the retail level, which obviously is not a surprise to anyone. Throughput is far more stubborn, in part because there aren’t enough digital products catering to the large-ticket usage, thus pushing people to cheques. Nonetheless, the trajectory has drastically accelerated with 30.8% of value now going through one of the four digital channels, witnessing the steepest increase of 9.89pps in full calendar year.

Mobile Banking

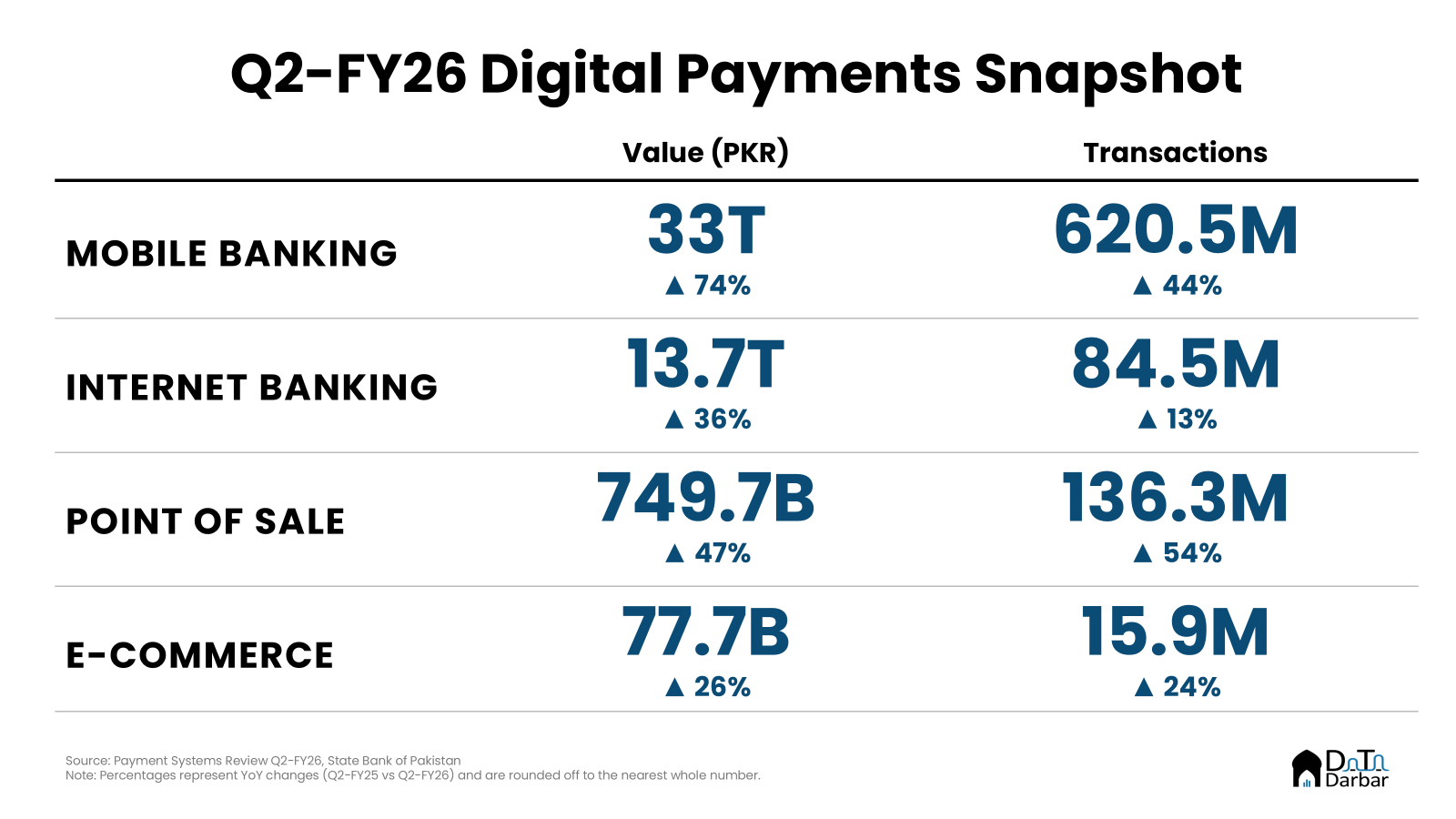

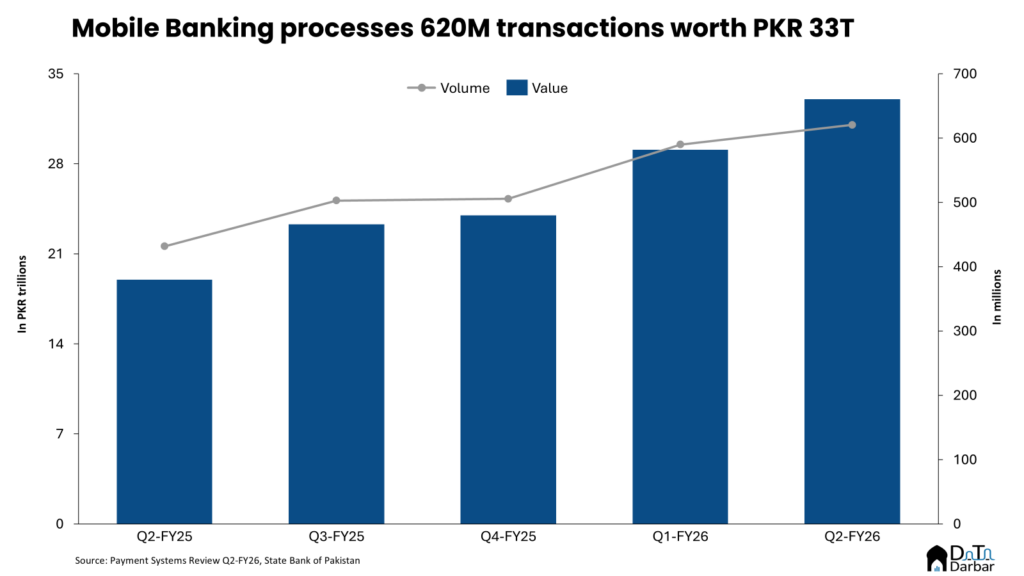

As always, mobile banking remained star of the show, boasting the highest quantum by far – 2x as much as the remaining three channels combined. In Q2-FY26, it processed throughput of PKR 33T across 620.5M transactions, up 74% and 44%, respectively. Consequently, on a 12-month basis, the value crossed the PKR 100T mark to PKR 109.4T while volumes breached the 2B threshold to 2.2B.

More importantly, the number of registered users hit 27.2M, increasing by 6.1M over the previous year – the steepest 12-month change since data is available. Similarly, the transaction sizes continue to get bigger, surpassing PKR 50,000 for the first time, which again is the biggest jump YoY.

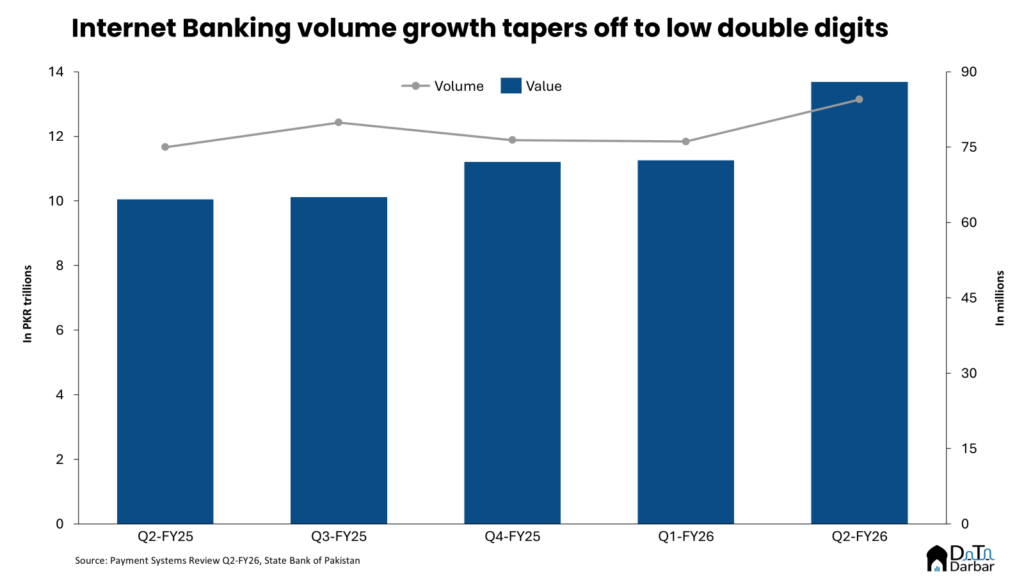

Internet Banking

In relative terms, internet banking seems to have a bad quarter, witnessing the slowest growth in volumes at 13%, clocking in at 84.5M during Q2-FY26. Throughput held up relatively better, jumping 36% PKR 13.7T, reaching PKR 46.3T on a TTM basis.

The path is quite clear: while mobile has become the channel of choice among retail audience, internet banking has become the preferred platform for businesses. Whether that’s because of a lack of choice or a natural inclination towards web apps is a whole another debate. Nonetheless, growth remained fairly strong, adding 2.5M users during 2025.

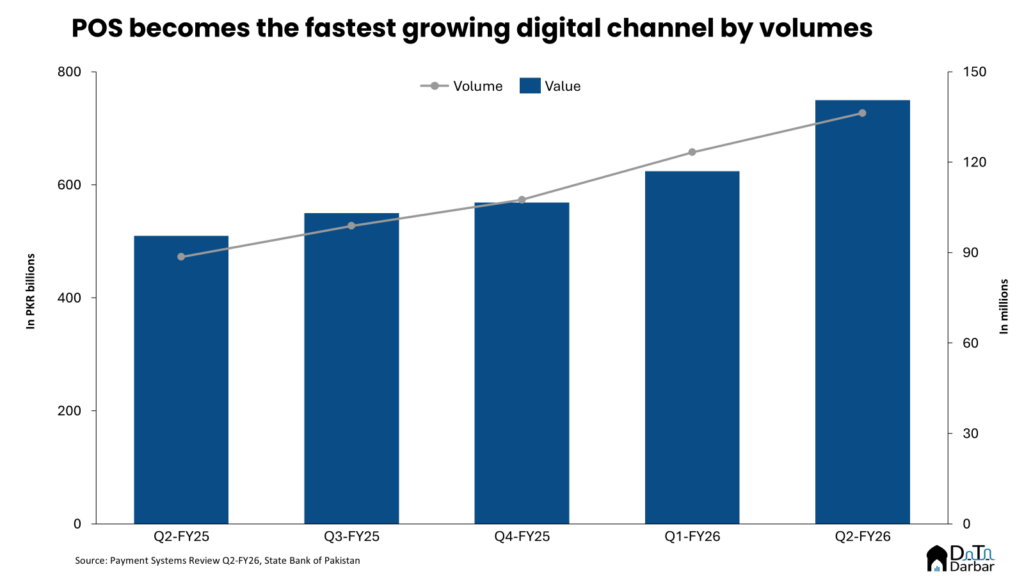

Point of Sale

On the hand, POS had a good run, becoming the fastest growing channel by volumes, which jumped 54% to 136.3M during Q2-FY26. At the first look, it may seem pretty nnormal but remember, this is the first instance since Q1’17 when POS has seen steeper rate of change than mobile banking. In all of 2025, the transaction count was 466M.

Throughput-wise, the growth was impressive at 47% in Q2, second only to mobile apps, as value approached PKR 750B. But the real story lies on the infrastructure side where the number of terminals reached 232K, up 53% YoY. The jump looks even better in absolute value: 80K+ machines were deployed in 2025 i.e. more than the total stock Pakistan had till September 2021. If anything, the space should heaten up even further in the coming months thanks to the ambitious acquiring targets set by the PM Cashless Initiative.

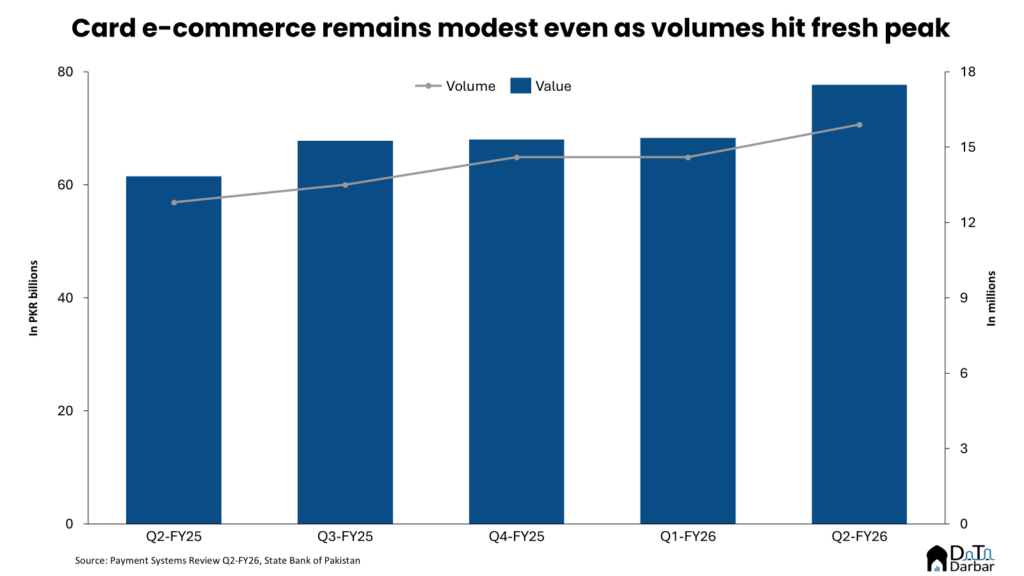

E-commerce

Forever the disappointment, card-based online commerce remained muted with throughput up 26% to PKR 77.7B in Q2-FY26, both the lowest among all channels. Nevertheless, volumes finally broke through and scaled to a fresh peak of 15.9M, taking the 2025 total to 58.6M.

Unlike transaction activity, acquiring infra showed actual signs of progress with the number of merchants registered with banks almost doubling to 17,449 by December 2025, from 8,932 12 months prior. Basically, it took just one year to equal the progress made in the preceding 8.5 years. Add to it the EMI universe and we are looking at a decent network altogether.

That said, it doesn’t even begin to scratch the surface of what branchless wallet-based e-commerce has managed, sitting around over a trillion rupees of throughput across almost billion transactions in the last 12 months. The idea here is not to compare the branchless universe with scheduled banking but rather how online commerce exists well beyond cards, which needless to say have seriously underperformed.

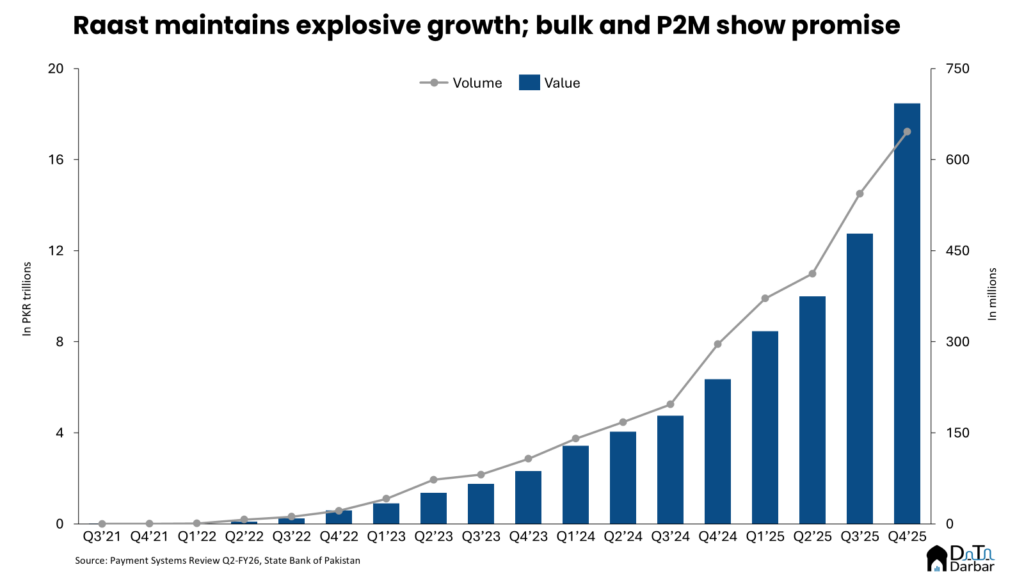

Raast

Things also picked pace at Pakistan’s national payment stack, Raast, which saw 645.8M transactions worth PKR 18.5T during the latest quarter, taking the 2025 aggregate to 1.97B and PKR 49.7T. It translates into YoY increase of 118.3% and 190.3%, respectively, with the former trending down albeit still in triple digits.

In absolute terms, P2P was by far the largest module processing PKR 15.7 trillion across 603M transactions with the average ticket rising to PKR 26,015. Yet, since the first full quarter of its launch, this was the lowest share for P2P, as bulk payments finally reached a meaningful scale of PKR 2.6T. But most importantly, it was P2M that finally had a breakout in its eighth quarter since launch: throughput clocked in at PKR 167.6B, from PKR 17B in Q1-FY26 while volumes stood came in at 33.6M, versus 4.3M. It’s still early days though and a lot more effort is needed to penetrate the retail economy.

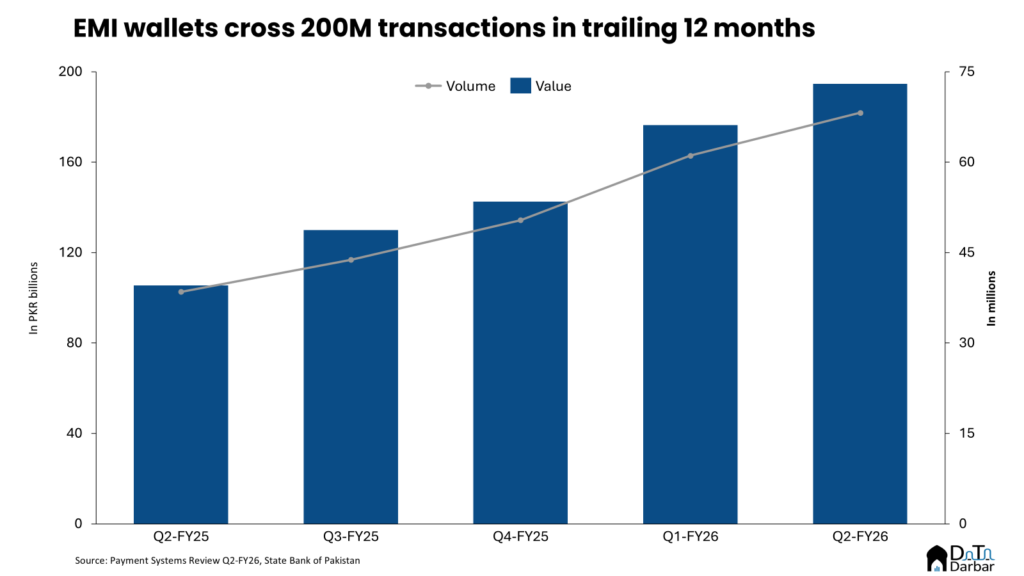

EMIs

Meanwhile, EMIs barely managed anything out of the ordinary. Transaction remained in line with past levels with rate of increase slowing down gradually and volumes rose to 68.2M worth PKR 194.6B in Q2-FY26. Both the scale and growth are rather mild considering how other newer modules/platforms have done. That said, the issuing side remained strong with around 2.1M new e-wallets opened during 2025 even as freelancer accounts flatllined.