In Pakistan, we have a habit of solving yesterday’s problems. Policy papers, strategy reports and op-eds routinely cite outdated data points, which are then recycled at conference panels, and now eventually parroted by AI bots. The result is not only lazy analysis but misplaced effort chasing the wrong solutions.

Financial inclusion is a good case in point. Ever since independence, Pakistan has been considered a laggard on this front, underperforming pretty much all countries of similar size. Unfortunately, the narrative today hasn’t changed even if the underlying data now paints quite a different picture.

Tracking progress: 70 vs 8 years

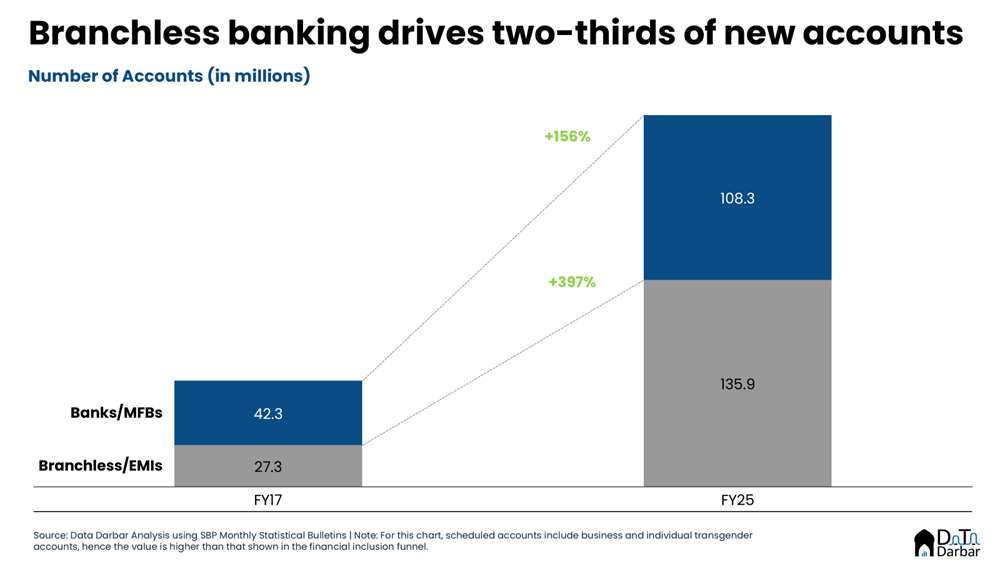

Between FY17 and FY25, Pakistan has witnessed a phenomenal improvement in financial inclusion levels with total accounts jumping 4x to reach 244 million, almost the size of our population. Just take a moment to appreciate how impressive this trajectory is: you’d be hard-pressed to find many areas with similar levels of progress in such a duration.

Over the last eight years, 174.5M+ financial accounts have been opened in Pakistan — i.e. just under 3x of what we managed in the first 70 years. And the credit largely goes to digitalization, with branchless and EMI wallets contributing two-thirds of all new accounts during this period.

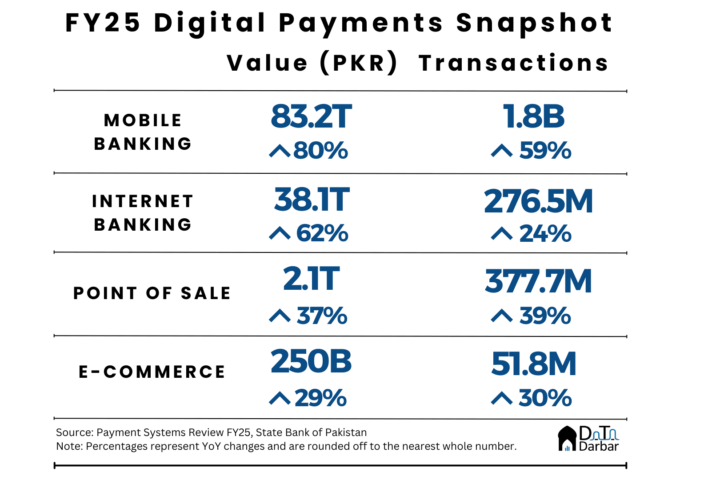

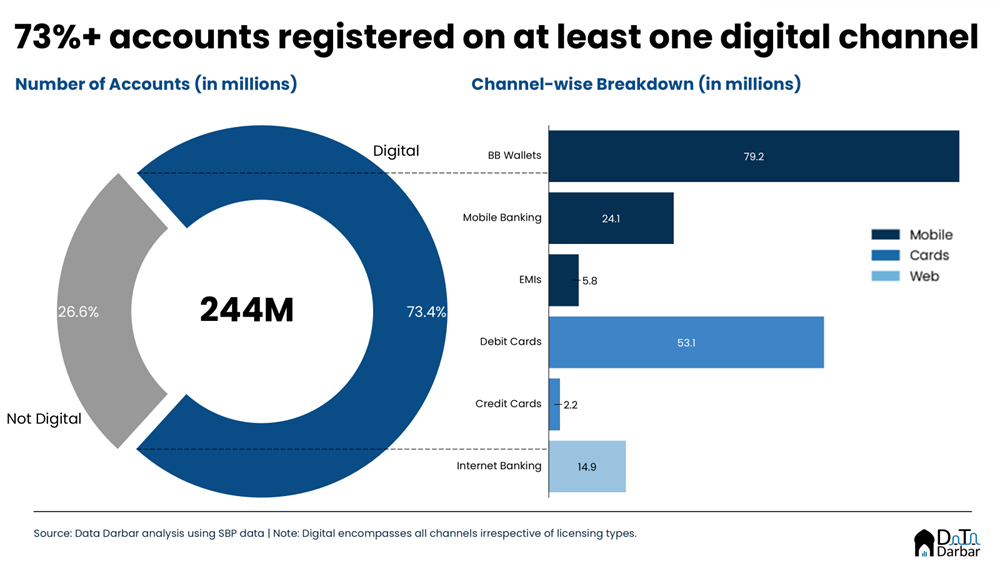

In fact, over 73% of all accounts are registered on at least one digital channel already. Unsurprisingly, mobile remains the dominant channel with 109M registered users across different licensing types as of FY25. Out of this, branchless naturally has the largest base of 79.1M (72.5%), followed by cards (55.3M) while internet banking is the smallest. When December 2025 data comes out, it’d only show further acceleration as we noted in the Q2-FY26 Payment System update.

Peeling the layers of financial inclusion in Pakistan

Now before any captain obvious warms up their fingers to point out, I understand well that the number of total accounts is not the right metric as it entails a high degree of duplication. A sizable segment of the population has multiple accounts across traditional banking plus the growing digital wallet options, hence inflating the figures substantially. Any single metric can ever be enough to properly measure anything as there are just too many caveats. The right approach is to think of financial inclusion as a funnel:

- total accounts → unique depositors → active depositors → transacting users

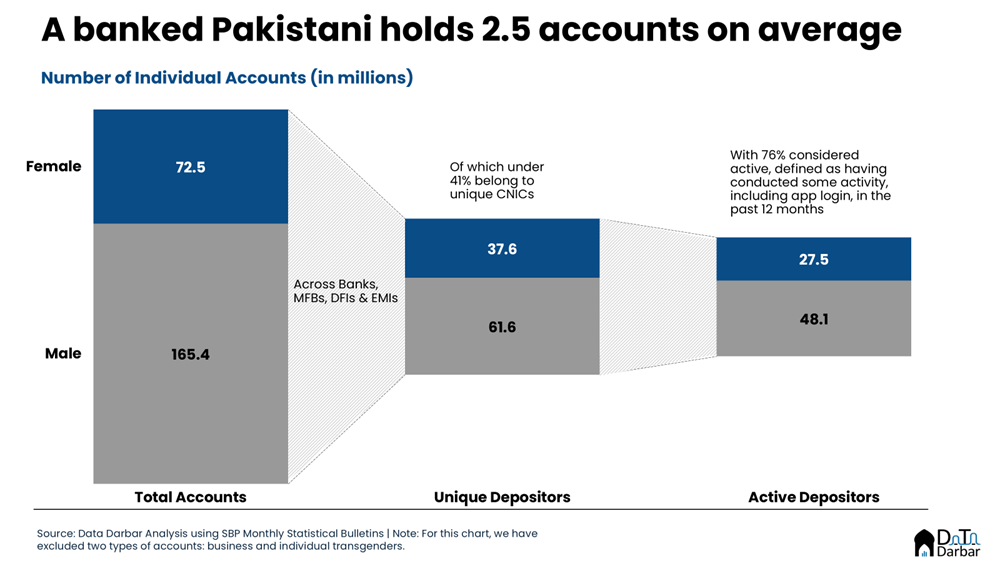

Then you need to dissect it by channel, segment, gender or other parameters to really understand what’s working and what’s not. Luckily, the data for the first three stages is available, that too gender-wise. Across banks, microfinance, development finance, and electronic money institutions, there are 99.2M unique depositors in the country — almost 40% of the headline figure. That’s still a fairly large number, but it puts the 244M in perspective and sort of punctures that.

Make no mistake, it still translates into 61% of our adult population, which includes anyone 15 or older as per the industry practice. That’s a bit unfair because financial services in Pakistan are centered around people over 18, though there are some product options for younger audiences too. However, this approach ensures consistency when benchmarking against peer markets.

The bigger problem is that the growth in unique depositors has somewhat lagged behind. Over the last eight years, the number has increased by 83%, well behind the 250% jump seen in total accounts. Essentially, while the base is still expanding, we are now seeing more deepening. Put it this way: as of FY25, a “banked” Pakistani has 2.5 accounts on average. Whether that translates into other products beyond payments or deposits is a discussion for another day.

Filter further for activity and the base shrinks again. The SBP defines “active” rather generously — having conducted some activity, including just an app login, in the past 12 months. Even by that low bar, only 76% of unique depositors qualify. That brings us to 75.6 million active depositors.

The Gender Gap

The gender split is where we still have much room for improvement, though recent data shows signs of promise. For starters, growth in female accounts has outpaced that of males, albeit on the back of a lower base. Among the 99.2M unique depositors, there are just 37.6M women as against 61.6M men. In absolute terms, the gap widens at each stage of the funnel: female active depositors stand at 27.5M versus 48.1M for males.

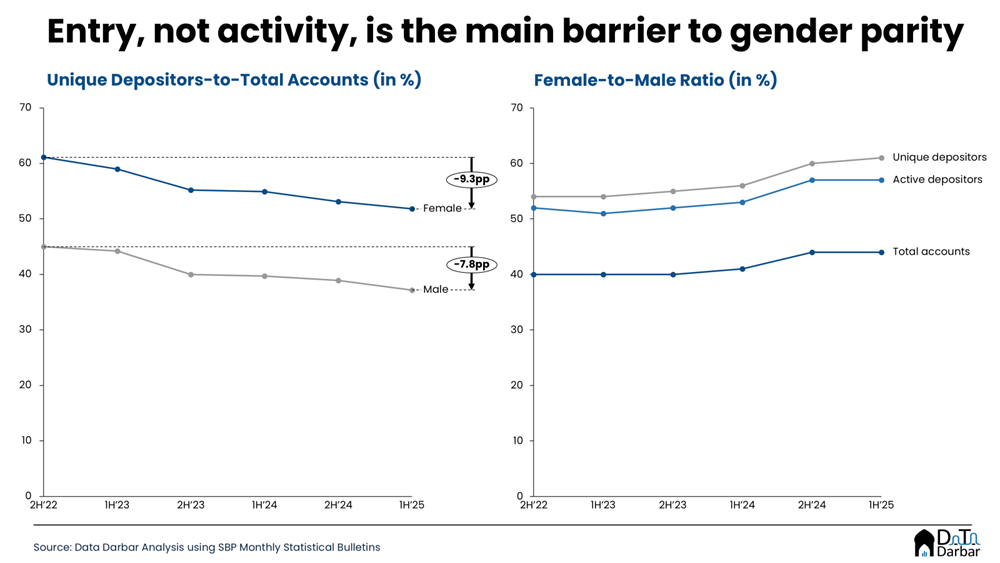

However, it might be more appropriate to measure this through a simple parity ratio i.e. dividing the relevant indicator for females by the corresponding value for males. At the total accounts level, the figure sits at just 44% as of FY25, though slightly improving from 40% three years ago. Unique depositors fare better at 61%, while active depositors sit at 57%. Similarly, women tend to have a higher rate of unique accountholders compared to men, despite both seeing a noticeable decline over the last three years.

Nonetheless, it is evident that female financial inclusion holds up better as you move up the funnel — whether against their own total accounts or compared to the corresponding indicators for men. The implication here is that entry, rather than retention or usage, is the bigger challenge when it comes to women. This is somewhat consistent with our previous research, which found that women have a relatively higher propensity to spend digitally.

Beyond Accounts

None of this is to suggest that the job is complete. Account-level indicators are, at best, loose proxy of financial inclusion and barely scratch the surface. The more meaningful yardsticks — transaction frequency, credit penetration, savings behaviour, investment access — tell a far less flattering story, as Pakistan continues to lag on most of them. However, addressing that end requires:

- a well-identified problem statement; and

- the right data to measure it against

It’s kind of a chicken and egg situation where the problem statement remains vague because the underlying data has major gaps, and the data gaps persist because those making decisions are looking at the wrong goal post. To break through this cycle, we need information at a far more granular level such as regional breakdowns, transaction activity, credit and investment penetration. Unfortunately, that’s an area where even acknowledgement, let alone progress, has been extremely slow to come by.